As you approach your 65th birthday, the countdown to Medicare’s Initial Enrollment Period begins ticking away. It’s a pivotal moment. Understanding the intricacies of Medicare enrollment isn’t just important – it’s essential. Failure to enroll on time could result in penalties. It is important that you understand your options and the penalties that may apply to you.

Whether you’re on the brink of eligibility or assisting a loved one through this process, arming yourself with knowledge is the first step toward securing seamless, penalty-free coverage. So, let’s embark on this journey together, navigating the maze of Medicare enrollment with confidence and clarity.

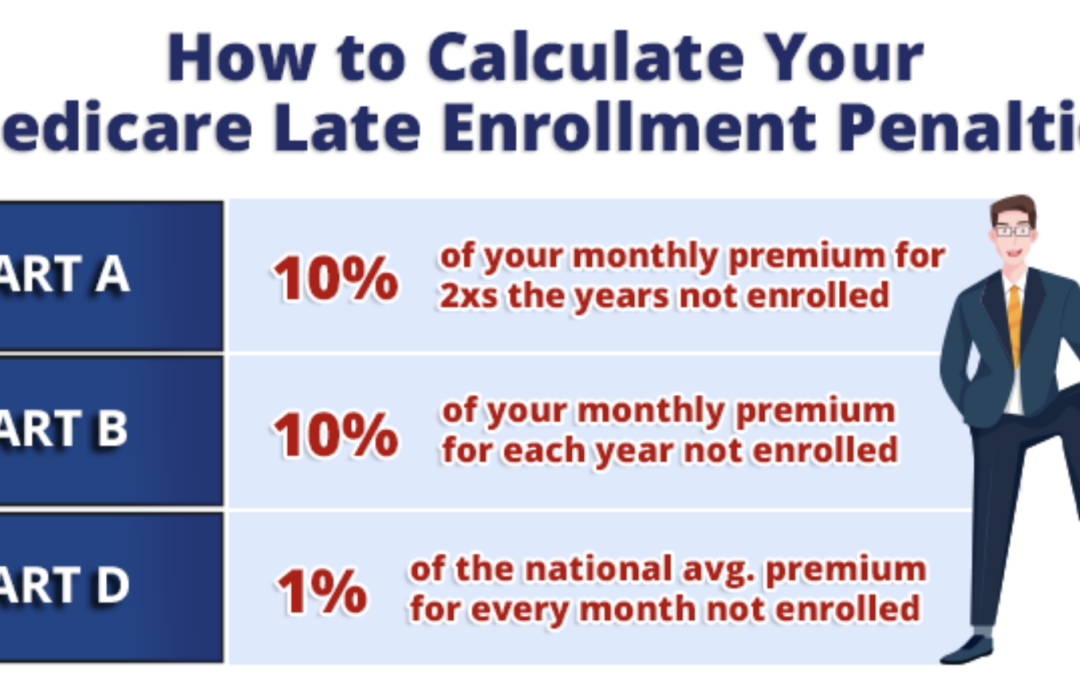

Part A – Hospital Insurance Coverage

Part A, also known as Hospital Insurance, provides essential coverage for inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services.

If you fail to sign up when you’re first eligible, you may face a penalty in the form of higher premiums. For each year that you could have had Part A coverage but didn’t enroll, your monthly premium could increase by 10%. This penalty persists for twice the number of years you were eligible but remained uninsured.

For example, if you were eligible for Part A three years ago but didn’t sign up, you’ll have to pay the higher premium for six years.

Part B – Medical Insurance Coverage

Similar to Medicare Part A, timely enrollment in Part B will prevent costly penalties and ensure comprehensive healthcare coverage. Part B, also known as Medical Insurance, covers essential services such as doctor’s visits, outpatient care, preventive services, and durable medical equipment.

If you don’t sign up during your Initial Enrollment Period, you may incur a late enrollment penalty, resulting in higher premiums for as long as you’re enrolled in Part B. This penalty accumulates at a rate of 10% for each full 12-month period that you could have had Part B coverage but didn’t enroll.

For instance, if you wait 27 months after your Initial Enrollment Period to sign up for Part B, your penalty could amount to a 20% increase in your monthly premium.

Part D – Prescription Drug Coverage

Medicare Part D provides vital prescription drug coverage, ensuring access to necessary medications to maintain your health and well-being. Enrolling in a Part D plan during your Initial Enrollment Period is essential to avoid potential penalties and gaps in coverage.

The Part D penalty is calculated based on the number of months you were eligible for Part D but didn’t have coverage. Specifically, the penalty amounts to 1% of the “national base beneficiary premium” for each month without coverage.

For example, if you were eligible to enroll in Part D but failed to do so for 27 months, your penalty would amount to a 27% increase of the “national base beneficiary premium.” In 2025, the base is $36.78. The penalty is then rounded to the nearest $0.10.

27% X $36.78 = $9.93

The monthly penalty for 2025 will be $9.90.

It’s important to note that enrolling in a Medicare Supplement Plan or an Advantage Plan does not exempt you from Part D penalties. Regardless of the type of plan you choose, the late enrollment penalty applies if you didn’t have creditable prescription drug coverage.

Exceptions to the Penalties

Exceptions to the penalty for late enrollment in Medicare exist, providing relief for individuals who had qualifying group health insurance coverage through their or their spouse’s employer during their Initial Enrollment Period. If you had such coverage when you were first eligible for Medicare, you may qualify for a Special Enrollment Period, allowing you to enroll in Medicare Part A and/or Part B without facing increased premiums or penalties. It’s important to understand and document any qualifying group health insurance coverage to ensure eligibility for these exceptions and avoid unnecessary financial penalties.

Even though IRMAA isn’t a penalty, you should be aware of these potential costs when enrolling in Medicare. IRMAA or Income-Related Monthly Adjustment Amount charges high income earners more for their Medicare.

Understanding the enrollment deadlines and penalties associated with Medicare Parts A, B, and D is essential for safeguarding your health coverage and financial well-being. We’ve discussed how delaying enrollment can result in increased premiums and gaps in coverage, emphasizing the importance of proactive planning and staying informed about eligibility criteria and exceptions. By arming yourself with knowledge and seeking assistance from knowledgeable brokers like HealthyMarks, you can navigate the complexities of Medicare enrollment with confidence and peace of mind, ensuring seamless access to quality healthcare without unnecessary financial burdens.

Keaton Marks is the owner and CEO at HealthyMarks including the medicare team. Keaton was born and raised in Encinitas. He often rode his bike through town and to the local beaches like Moonlight. Keaton knows it is important to have a local resource, someone who understands the area, the hospitals and networks of doctors. Keaton is proud to be a local Medicare broker who is able to assist the people in his town when selecting medicare plans.

Keaton believes one thing above all else: “Medicare is confusing… but it doesn’t have to be! That is where HealthyMarks Medicare comes in” Please contact me with any questions.